COVID Stock Winners Have Round Tripped - What Does it Mean for Real Estate?

The monetary policy response to COVID-19 was beneficial for most asset classes, given near 0% interest rates tend to drive investment and risk-taking. This dynamic was very obvious in technology stocks (as defined by the Nasdaq), cryptocurrencies, and real estate. In fact, real estate was the best-performing asset class on a risk (volatility) adjusted basis in 2021 with a Sharpe ratio of ~3 (as calculated by return/volatility).

Parcl Team

Oct 20, 2022

The monetary policy response to COVID-19 was beneficial for most asset classes, given near 0% interest rates tend to drive investment and risk-taking. This dynamic was very obvious in technology stocks (as defined by the Nasdaq), cryptocurrencies, and real estate. In fact, real estate was the best performing asset class on a risk (volatility) adjusted basis in 2021 with a Sharpe ratio of ~3 (as calculated by return/volatility).

COVID also produced a massive tailwind for a specific subset of companies who benefitted from behavioral shifts caused by the pandemic - primarily, work from home (WFH). While this tailwind was particularly evident in technology stocks like Zoom and Shopify, it was also prevalent in real estate, especially in certain regions, as people migrated to geographies with lower housing costs, more favorable tax regimes, and better climates (like Miami).

In the below discussion we explore the impact of COVID on real estate and draw analogies to the stock market

Key takeaways:

Most COVID beneficiary stocks are now at or below 2020 levels

If Real Estate follows suit - COVID relocation winners could fall 50%+

Drawdowns happen much faster than recoveries

The case for a soft(er) landing is compelling given the dis-incentive to sell properties with lower mortgage rates

Most COVID beneficiary stocks are now at or below 2020 levels

2022 has been a volatile year for many assets as inflation and the resulting monetary policy (i.e. higher interest rates) has become a large headwind to markets. Markets have entered into bear territory and many high growth software stocks have completely retraced all COVID gains.

COVID beneficiaries have been hit particularly hard because of two factors:

Higher interest rates are impacting valuation

There was a pull forward of demand during COVID and now some or all of this excess demand is receding

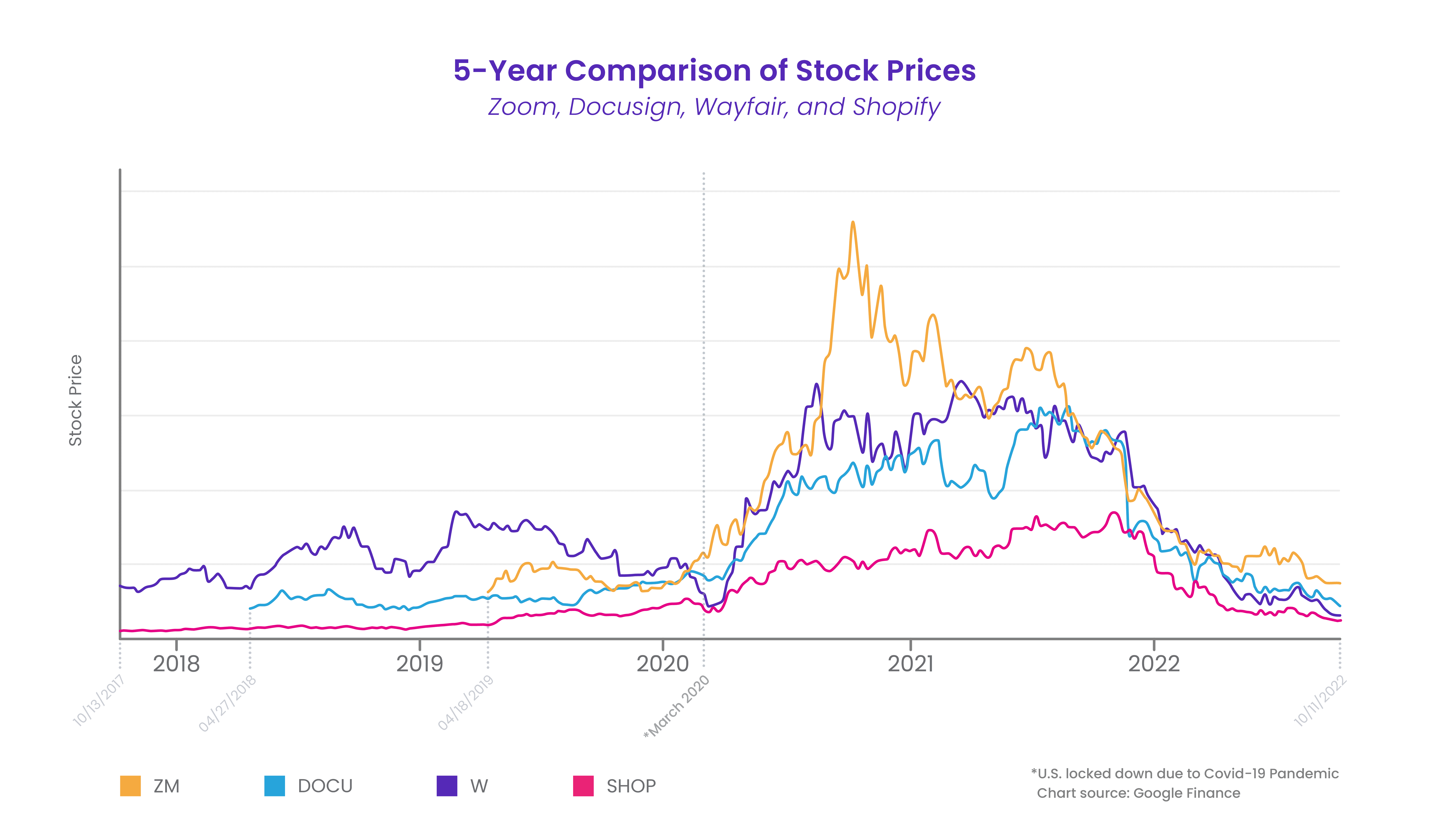

In the below chart, we look at the five-year stock performance of what we view as four key COVID winners: Zoom (video conferencing), Docusign (digital signature), Wayfair (affordable home furniture), and Shopify (e-commerce). Each has completely retraced all gains from COVID (March 2020) even though at least some portion of consumer behavior is permanently changed.

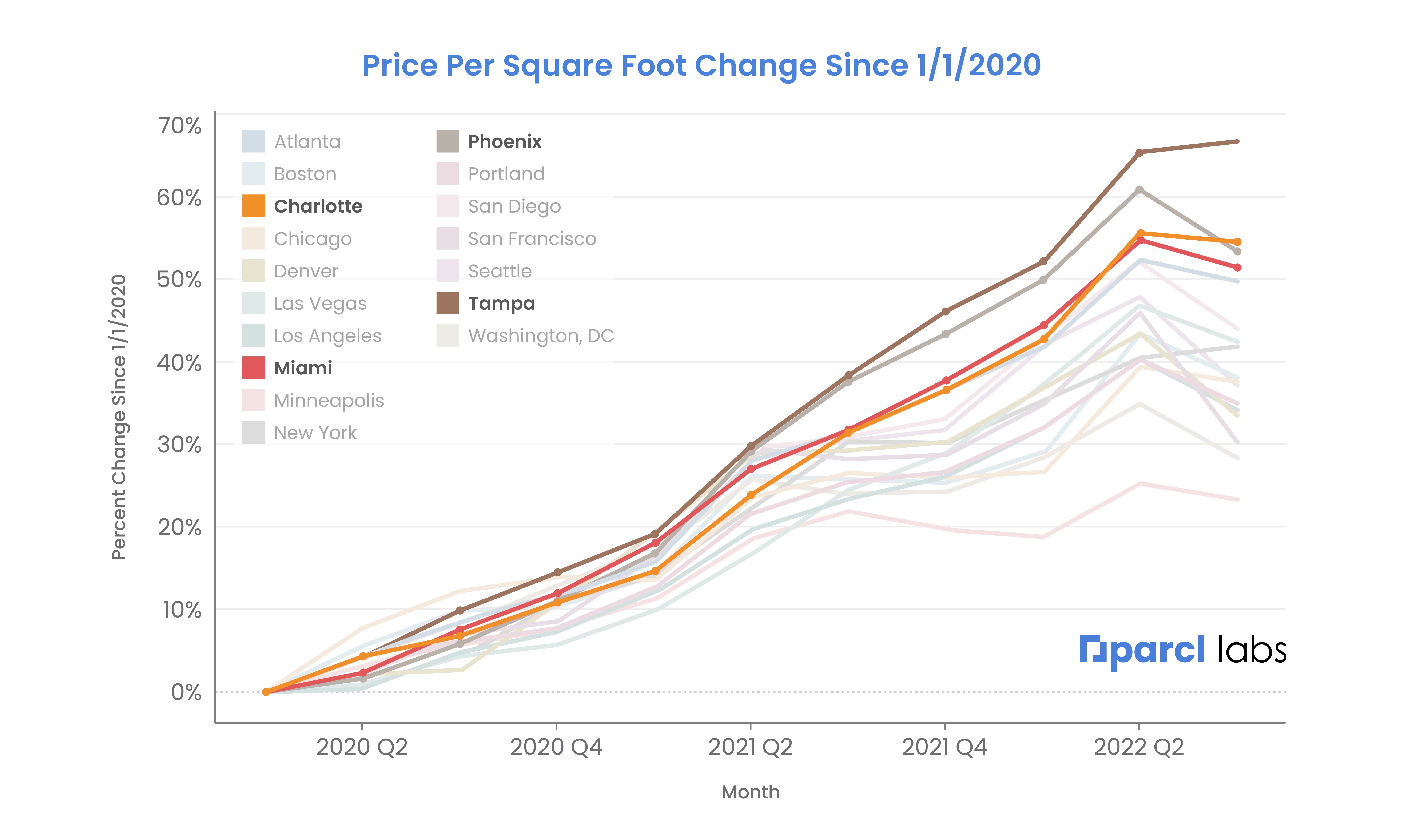

If Real Estate were to follow suit - COVID relocation winners could fall 50%+

In that vein, we wanted to explore where the COVID real estate winners stood with respect to price performance and what a drawdown could look like should they retrace their COVID gains. Using Parcl Labs data, we explored the four largest COVID winners within the top 20 MSAs in the USA; Tampa, Miami, Phoenix, and Charlotte. On average, these cities were up ~60% from 2020 and peaked in 2Q22. While the market price per square foot in these cities has been somewhat resilient in recent months, its starting to decline at a faster pace in recent weeks.

Using the COVID stocks above as an analogy, if these real estate markets were to retrace their COVID gains, we believe there would be as much as 50% downside in each of these cities on a price per square foot basis.

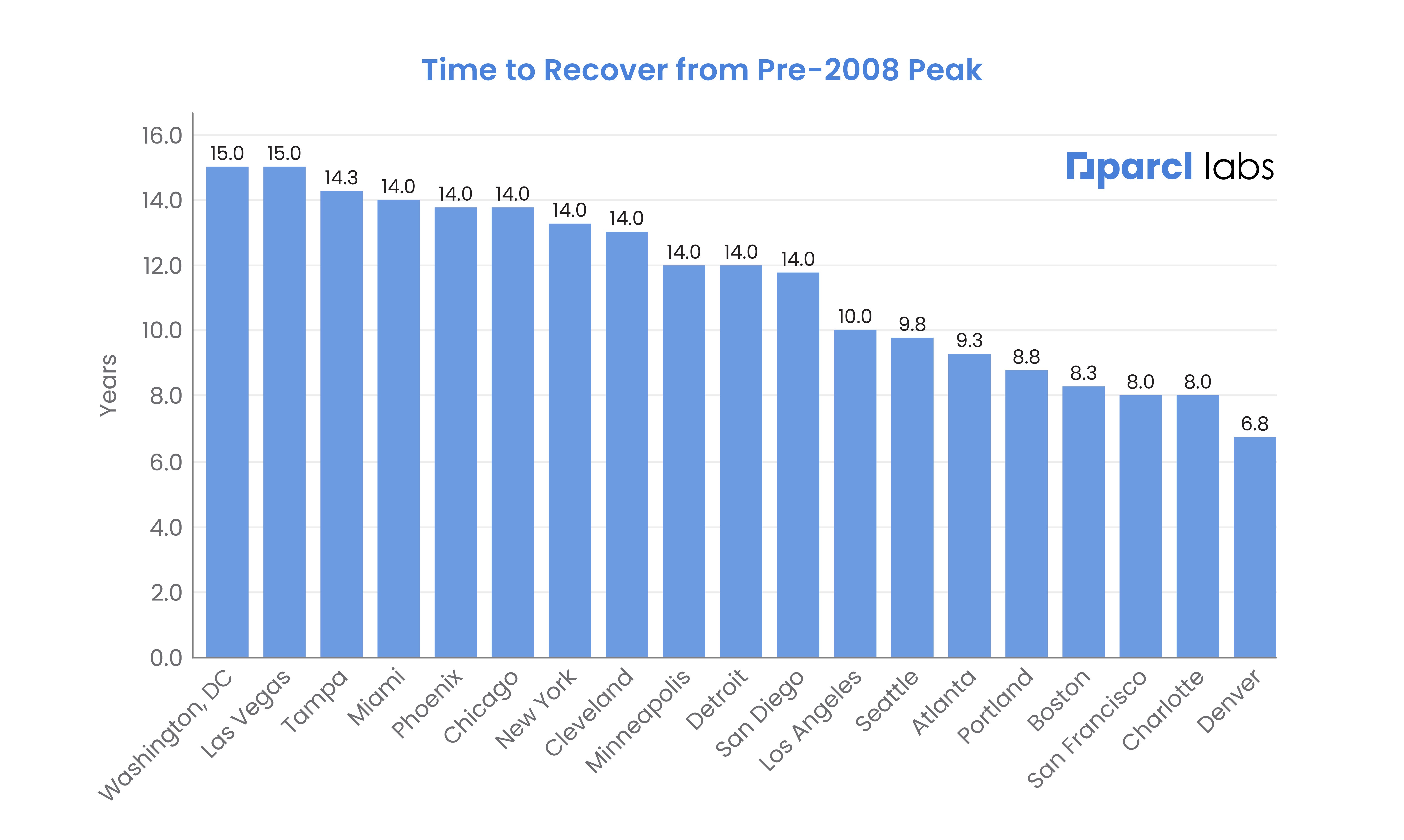

Drawdowns happen fast, recoveries happen slow

We continue to see asset prices, particularly stocks, bleed lower, and within the last 2 months, home prices have begun rolling over at the national level. For real estate we see further risk to the downside given higher mortgage rates, seasonality (fall/winter), and a weakening economy.

Generally speaking, sharp downside price movements happen quickly and can be violent. Recoveries can take much longer. In the chart below, we show how long its taken to get back to pre-2008 levels. In many instances, these markets have just reclaimed their prior peak (not unlike technology stocks post 2000) - and if adjusting for inflation many of these cities haven’t recovered at all.

The case for a soft landing is nuanced but compelling - the story of the 3 vs 7 percenters

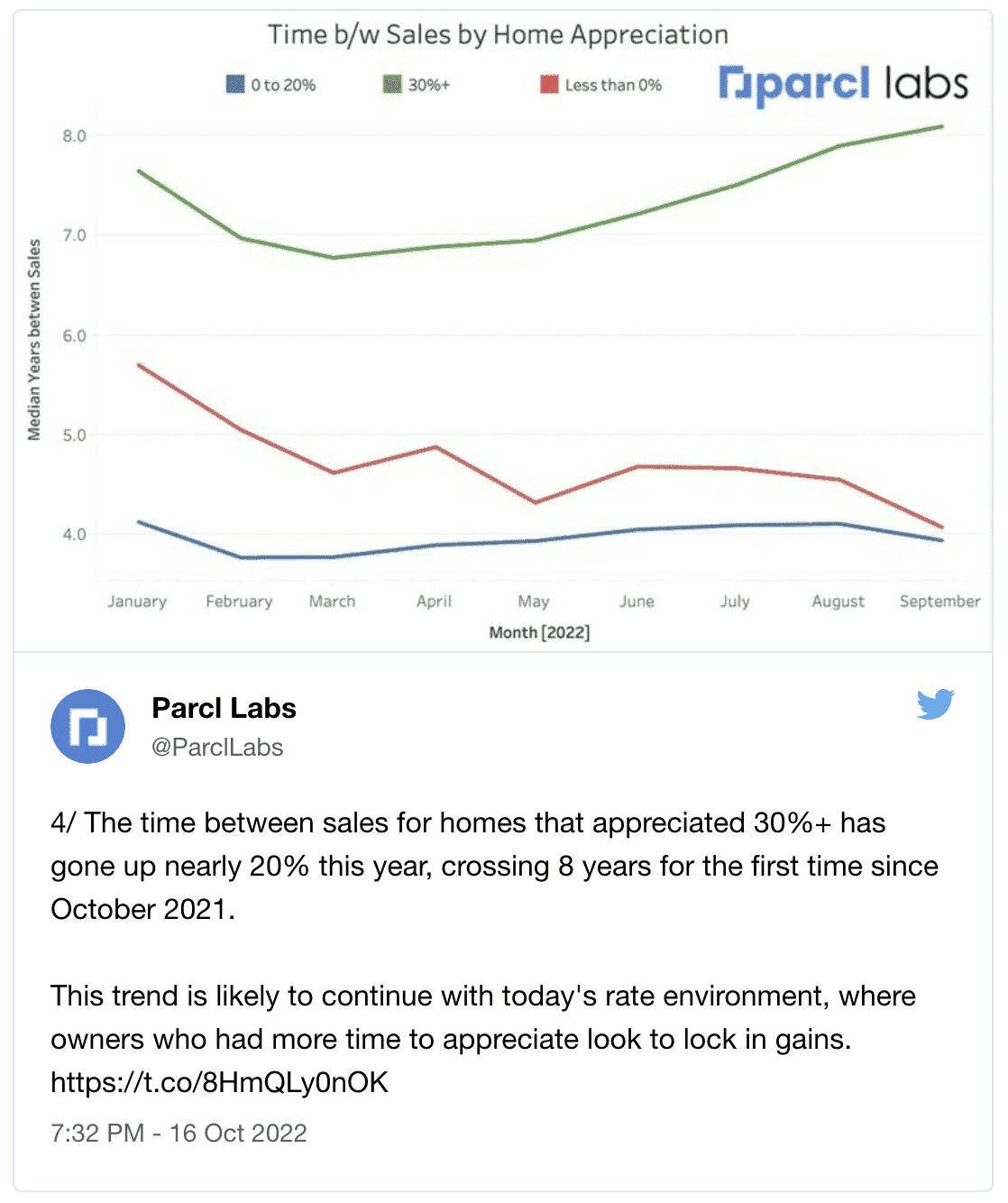

Some good news? We see reason to be optimistic for a soft landing in real estate - however, the magnitude of how soft is unclear. The reasons for this optimism are nuanced. Over the last 10 years, the average mortgage rate has stayed within a tight range of about 3% to 4%; we’ll call the people that pay this rate on their mortgage “the 3 percenters”. Within just four months, mortgage rates are now 7%+ - we’ll call the people that obtain this new rate “the 7 percenters”. 3 percenters have very little incentive to sell their homes, as any new home would come with a much higher mortgage payment. In short, 3 percenters shouldn’t want to become 7 percenters. Unless, of course, realized gains can comfortably offset the much higher monthly payment. Note that we are beginning to see high appreciation (i.e. well in the money) inventory come on line - most notably from owners that purchased over 8 years ago. This high appreciation inventory is currently driving the bulk of sales in the market. Parcl Labs recently tweeted about this dynamic

As such, we expect that there will be limited supply of existing homes on the market which, on balance, could limit price downside. That said, new homes on the market will likely be discounted to current prices given a) homebuilders generally have greater sensitivity to duration than do individual owners of existing homes and, 2) a new home purchase requires any potential buyer to take on the aforementioned 7% mortgage. Of course, should the economy head into a deeper recession, we could see more forced selling across all home types, which would accelerate price action to the downside.

The 3 Percenters: individuals who has a mortgage rate between 3%-4%

The 7 Percenters: individuals who has a mortgage rate at 7%+

The need for actionable, real-time real estate insights is higher than ever

\It is clear to us that residential real estate is in need of a new source of representative, timely and normalized pricing data. A reliable, single source of truth would not only help investors and intermediaries gain market exposure, uncover unique insights and mitigate risk, but it could also prove invaluable for government policymakers and research agencies implementing agendas based on timely and geographically specific real estate trends.

Parcl Labs has created a real-time real estate data analytics platform to adapt to any level of geography and context. The goal is to empower users with the highest quality data and insights to ensure real estate decisions are driven by correct, accurate, and real-time data.

Parcl Price Feeds and the Parcl Protocol will provide real-time, representative, and comprehensive residential real estate pricing and enable a liquid market for real estate exposure, for the first time, ever.

Shared content and posted charts are intended to be used for informational and educational purposes only. Parcl does not offer, and this information shall not be understood or construed as, financial advice or investment recommendations. The information provided is not a substitute for advice from an investment professional. Parcl does not accept liability for any financial loss or damages. For more information please see the terms of use.

Parcl Team